This week brought us new data points on vehicle sales, PMI, and factory orders. With this data, the final average for February is complete and we have advance estimate for March:

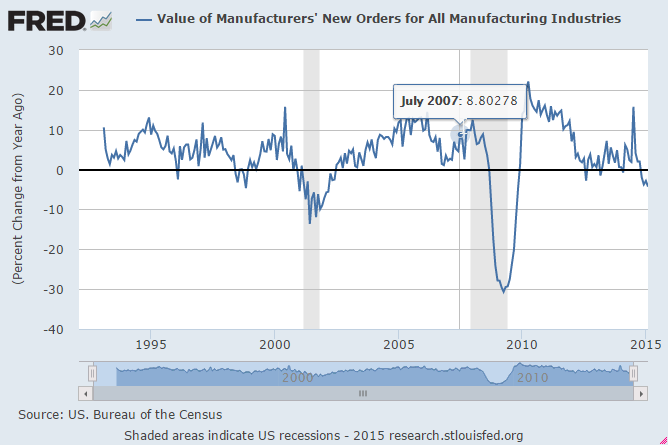

The data looks weak. Especially factory orders are in the recessionary range:

Other areas such as vehicle sales and construction show some weakness but are still growing yoy. Overall, economy is much weaker than stock market. This is also seen in the US Growth Barometer:

How long can the divergence between economic data and stock market continue? Short answer is that the stocks go up as long as there is price momentum but the momentum may be fading. Below is the plot of SP500 and RSI. Notice the similarity of current situation to prior tops. The divergence between RSI and price is now extended beyond the prior peaks.